Trade the Markets 06-22-2009

admin on 06 22, 2009

“Monday, Monday…â€

Monday mornings have been some of the most interesting times in the market over the past few months. It seems that we’re commenting on either a sizable gap to the upside or downside at the start of every week. Today has brought us another downside gap of significance. We put out a rather lengthy market update video over the weekend about where we “think things are†right now. These are very interesting times. Geopolitics are now stealing most of the headlines that we’d guess the illusionists had planned for more talk of “green shootsâ€. The list goes on and on but the BRIC countries and the Japanese providing “happy talk†publicly as they are probably running for any and all exits of the US dollar would rank at the top of our list for sell catalysts. The movie theater is on fire but “remain calm, all is well†they tell us while slinking towards the periphery. “Thanks guys!â€Â But quite honestly, who can blame them? They see what our central bank and federal government are up to and the ludicrous scale that they’re now working with. They know what it portends. They effectively know they’ve been “hadâ€. If there weren’t a short-term cost to refocusing significant portions of their economies away from the US consumer it’s likely that they’d have been long gone already. Clearly they can receive a much better return than they would here in the US. It’s not hard to beat interest payments that will lose vs. inflation and principal returned via in the form of a significantly devalued currency. All of this “currency stuff†is meant not to discount Al Qaeda via Pakistan’s nukes and of course N. Korea with their own variety actively threatening the US with warfare-like chatter. Oil and the precious metals are in full scale retreat as the market is cracking and the tensions are rising, especially in Tehran. Let’s not forget to mention that Goldman Sachs appears to be very close to reporting record profits and thus record bonus payouts for the first half of 2009. With US economic conditions still officially deteriorating, albeit at a slowing pace, we doubt that the average US citizen will welcome the GS news wholeheartedly. This could finally be the time when it starts to sink in across the board that regardless of which of the two major parties holds sway in D.C., the bankers and Wall St. finscamciers are always taken care of in the end to the great expense of the taxpayer. The average taxpayer cant’ count on bailouts, loans, the ability to write legislation and dictate policy nor do they have a direct line to prime movers so that they’ll know tomorrow’s news last week. Goldman just happened to hit their stride trading-wise over the past 9 months, right? The financials all needed to raise capital through stock offerings and lo and behold a historic rally ensues in the nick of time followed by green shoots happy talk ad-nauseum and almost magically they’re all exchanging shares for cash but often at price levels that are up 200 to 300% from where they were only WEEKS ago. We wonder if the big Wall St. firms were able to make any money in and around and through that action…. The world may never know…

We’re sticking with what’s worked for us over the years and that is “keeping our eye on the ballâ€. We’ve yet to see significant hiring of any meaningful kind and with more and more workers having employment difficulties the likelihood that things are really improving is low. The viscous cycle of declining construction, declining home prices, worsening employment conditions, and riskier mortgage terms coming due is only being compounded by the absurdities coming out of the federal government. Just as we asked the question “If GM can’t make it with 2 consecutive bubble booms in which they sold high margin SUVs like hotcakes, then under what conditions can they make it?â€, we now ask, “If we couldn’t afford all of the Bush and Republicans at the helm out of control spending, then how can we now quadruple that and afford it with a seriously weakened financial state of affairs across the board?â€Â Dramatically adding federal government weights to the backs of average American during difficult times like these seems about as foolhardy as it gets to us. Who knows? Maybe Bismarck will be proven prescient yet again. Let’s hope so:

“God has a special providence for fools, drunks, and the United States of America.â€

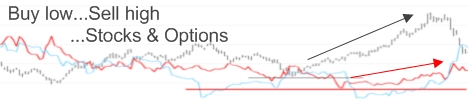

The Technical Picture:

This is our technical picture from 2 weeks back that we’re reprinting:

We’ve switched our color scheme around on this SPYs chart. It seems as though quite a few folks didn’t care for our white backgrounds with vibrant colors. Hopefully this will work better for them. We’ve kept the labeling to a minimum too as that was apparently getting in the way of the picture for too many readers as well. This is mainly a breadth chart that we review regularly. There isn’t a screaming sell signal at this point but we think that it’s clearly a time to expect a consolidation if not more. The momentum of the market seemed to wither somewhat last week. The market was unable to reach our projections so that tells us that things are either “over†for now or will take a little longer than we anticipated. We have a horizontal support line in RED that we’ve identified as our secondary support if the GRAY support line is penetrated. Our view is that we need to see how things are shaping up should the market head to these levels as we’d expect them to at this point.

Here’s this week’s picture:

We referenced our picture from 2 weeks back because things have only gotten worse and it now looks like the time we alluded to at the end of those comments is well upon us. The maelstrom of variables, of which we only ticked off a few in our opening comments, seem to be forcing this market towards support levels in a hurry. In the DOW we see 8200ish followed by 7950ish follow by 7700ish as the “step down†levels. We’ve been looking for a 10% correction from the highest highs and 7950ish just about fills the bill for the DOW.

The SPYs however have a little bit different of an outlook. We’ve noted $87.50 and $82.50 coincidentally on the SPY chart. $87.50 would more or less provide us with the 10% correction we’re looking for and obviously $82.50 would be a good deal more. With as many “balls in the air†though that there are right now, we won’t eliminate the possibilities of anything. Earnings reports will soon be coming fast and furious along with forward looking commentary. And perhaps, most importantly of all, we’re only a day or two from a succession of Treasury debt auctions that are historic in size. How they “go†and how the results are “treated†by our market-moving friends could be very interesting indeed. That’s why as bad as things look this morning we won’t rule out epic short squeezes even as we believe that the correction should have further to run all things considered.

Popular Posts

Recent Posts

Recent Comments

- CheapIV.com » Why You can Throw Traditional Diversification in the Trash: ... have spent their

- Tim Geithner – China’s Laughing Boy - Trade the E-minis: ... Learn how Timmy

- Tim Geithner – China’s Laughing Boy | Notes from the E-mini Trading Professor: ... Learn how Timmy

- Swing Trading Stock: ... Learn Timmy Next

- Timmy Geithner has Cried “Wolf” Too Many Times | THE ART OF EXCESS: ... Learn how Timmy